Fixed Income Perspectives: Themes for 2H24 – Volatility is a Ladder

Eric Stein, CFA

Head of Investments and CIO, Fixed Income

As we approach the halfway point of the year, all eyes remain on Federal Reserve policy and the pace of inflation’s downward trend.

Central banks are becoming more dovish, but when will the much-anticipated rate cuts materialize? We’ve identified six key themes we believe will influence the Fed and impact investors in the second half of 2024. Spoiler alert: Periods of volatility are likely and will provide opportunities to episodically add risk.

1 AI spend supporting positive macro outlook

Investment in AI technology and infrastructure will continue to accelerate, supporting both near-term growth and long-term gains in efficiency, despite some inefficient capital deployment along the way. Customer service and communication related labor will increasingly be replaced by capital investment, shifting power to capital and exacerbating inequality.

2 Consumers and fiscal policy supporting U.S. growth

The wealth effect will continue to support consumer spending, even as slowing wage gains and high prices weigh on low-income consumers. The resulting solid aggregate consumption and still supportive fiscal policy will keep growth near trend, despite higher capital costs curbing private investment.

3 U.S. inflation trending lower

Moderating wage growth and the lagged impact of the decline in rent prices will allow inflation to trend lower, but resilient services spending and ‘regulated market pricing’ dynamics will keep inflation above the Fed’s target. Overcapacity in China will keep goods prices in deflation with periodic volatility arising from geopolitical disputes.

4 Global growth balancing out

Europe and China have bottomed, and will contribute positively to global growth, driven by local consumption and trade respectively, offsetting the slowdown in U.S. Spending on national and economic security will initially support growth, however this will divert funds from productivity enhancements, ultimately degrading potential growth and exacerbating debt burdens.

5 Central banks getting more dovish

Decelerating inflation will allow major developed market central banks to reduce policy rates. Increasing pressure on lower-income consumers from slowing wage growth and still-high prices for rents and other necessities will allow the Fed to begin quarterly cuts before the election, though the now-higher neutral rate will ultimately limit the extent of the easing. The abatement of supply shocks will allow the ECB to deliver a longer easing cycle than many counterparts. Emerging market central banks will be pressured to cut more than expected once the Fed begins easing policy.

6 Markets: Seizing opportunities

Duration-oriented risks are poised to benefit from the implementation of central bank policy and the resulting decrease in rate volatility. Strong fundamentals will continue to support tight spreads, while periods of volatility spurred by expectations of lower growth and post-election policies changes will provide opportunities to episodically add risk.

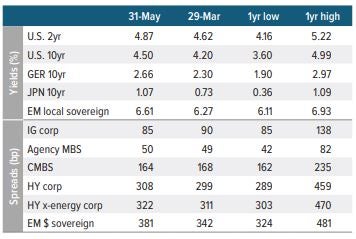

As of 05/31/24. Sources: Bloomberg, JP Morgan, Voya IM. See disclosures for more information about indices. Past performance is no guarantee of future results.

Sector outlooks

Investment grade corporates

- Overall, the macro backdrop is supportive of investment grade corporate fundamentals.

- Quarterly earnings continue to exceed analyst estimates with tech companies leading the way.

- New issuance was above average in May but continued to trend down from the higher levels earlier in 2024, which provided some relief on the technical side.

- From a positioning standpoint, we remain overweight financials, BBBs and the 10-year part of the curve.

High yield corporates

- While higher interest costs are beginning to weigh on credit quality, defaults and credit stress remain limited.

- The fundamental backdrop remains supportive for credit, but there is significant tail risk in stressed business models.

- From a positioning standpoint, we are overweight food/beverage, builders/building products, healthcare/pharma and energy. We are underweight technology, as well as media/telecom companies with structurally challenged business models.

Senior loans

- Senior loans posted a positive return in May, bolstered by both interest carry and market value changes.

- With over 60% of loans trading above par, the primary market saw another wave of repricings in May, with monthly volume reaching a record of $119 billion.

- While corporate earnings are solid, there continues to be dispersion among issuers and sectors and we maintain cautious sectoral views and up inequality positioning.

- We are cautious on cyclical sectors and those reliant on discretionary consumer spending. We are also underweight the B- and CCC-rated segments of the market.

Agency mortgages

- While May prepayment speeds are expected to increase, the general backdrop for prepayments is expected to remain muted due to a slow housing market and dampened refinancing activity.

- The performance of agency mortgages will be closely correlated with overall volatility and rate directionality in the near term.

- Longer-term, fundamentals and the supply environment favor the asset class for 2024.

Securitized credit

- Usually, we’d look to traditionally higher beta sectors/sub-sectors to lead in an “everything rally” (like CRT and CLOs). However, the rally in rates that is currently on display is such an important piece of the CMBS outlook, we’d expect that beleaguered sector to continue to lead, at least in the near term.

- A vibrant new issue market suggests sizeable and deep interest across SASB and conduit markets, which indicates strong momentum for risk holders in this sector.

- CLOs, conversely, which have enjoyed the higher for longer, inverted curve dynamics from an income perspective, may be more vulnerable as we progress in the Fed’s monetary policy regime. Coupled with extremely high issuance and spreads that have rallied considerably, we are dubious on this sector’s ability to continue to lead into this leg of the rally.

- In ABS and non-agency RMBS, we like these sectors’ prospects to contribute to outperformance potential. While we don’t see the catalyst for either to lead from an asset allocation point of view, look for them to enjoy steady sponsorship and deep liquidity as strong fundamentals fuel risk appetite across a wide range of macro scenarios.

Emerging market debt

- Emerging market (EM) central banks will likely be more cautious going forward, but historically elevated real rates should allow for room to move domestic rates lower.

- While China’s latest policy response appears to have stabilized the country’s economic activity, housing and private sector confidence remain weak and growth is likely to slow.

Absolute yield levels remain attractive relative to historical levels, and we continue to find the most attractive opportunities in LatAm corporates.

A note about risk The principal risks are generally those attributable to bond investing. All investments in bonds are subject to market risks as well as issuer, credit, prepayment, extension, and other risks. The value of an investment is not guaranteed and will fluctuate. Market risk is the risk that securities may decline in value due to factors affecting the securities markets or particular industries. Bonds have fixed principal and return if held to maturity but may fluctuate in the interim. Generally, when interest rates rise, bond prices fall. Bonds with longer maturities tend to be more sensitive to changes in interest rates. Issuer risk is the risk that the value of a security may decline for reasons specific to the issuer, such as changes in its financial condition. |