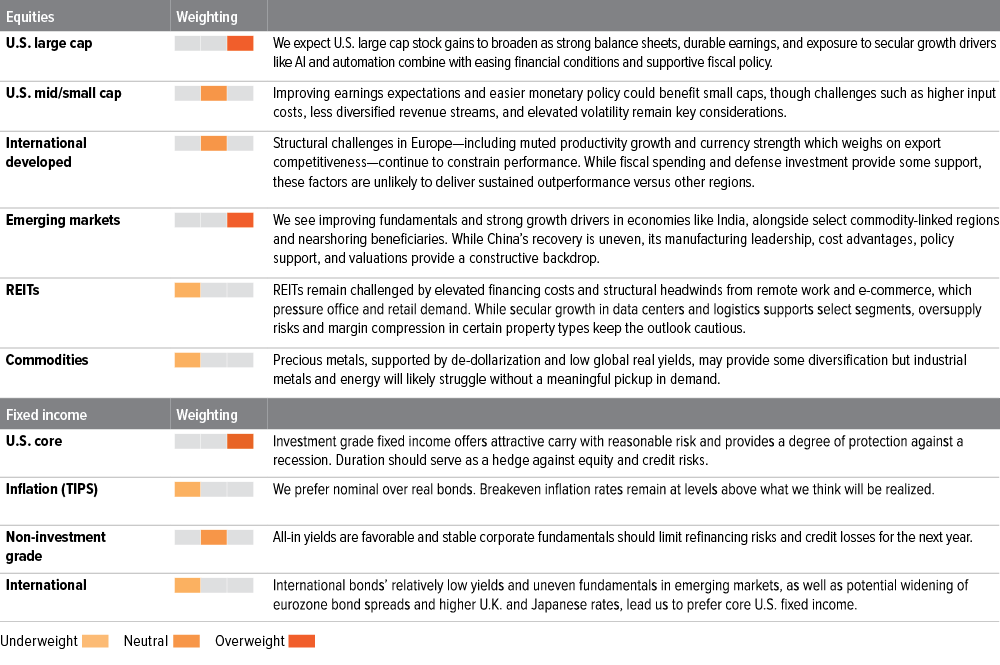

Multi-Asset Perspectives: Shifting from U.S. Dominance to Global Balance

CIO, Multi-Asset Strategies and Solutions

Improving global equity fundamentals and valuations argue for a more balanced approach.

Quick take

Equity fundamentals remain supportive, underpinned by continued economic expansion, easing inflation pressures, and sustained investment in productivity‑enhancing technologies such as artificial intelligence (AI) and automation. Corporate balance sheets are broadly healthy, financial conditions—supported by gradual monetary easing—continue to favor risk assets, and earnings growth remains positive.

After several years of pronounced U.S. equity leadership, fundamentals outside of the U.S. have improved, supported by firmer growth dynamics, selective fiscal support, and more attractive valuations relative to elevated U.S. multiples and historically high market concentration. U.S. large cap equities remain a core allocation given their exposure to innovation, durable cash flows, and structural growth themes. We favor a diversified global equity allocation that offers a more balanced and compelling risk/ return profile than a U.S.-centric stance driven by a narrow set of factors.

Market indicators

Economic growth (moderating)

U.S. real GDP grew by 2.3% year over year in 3Q25. The government shutdown likely slowed 4Q25 GDP growth, but it should bounce back as impacts reverse and policy stimulus begins to kick in.

Fundamentals (positive)

3Q25 year-over-year S&P 500 earnings grew by nearly 15%, with 9 of 11 sectors growing earnings.1 Technology and financials led, while the energy and communications sectors lagged. 4Q25 earnings are currently expected to show growth of about 9%.

Valuations (stretched)

U.S. equity valuations remain elevated, particularly for large cap stocks. However, when adjusted for profit margins, prices seem more justified. Non‑U.S. valuations remain lower, but multiple expansion drove more than half of 2025 returns for international equities, whereas S&P 500 performance was driven primarily by earnings growth.

Sentiment (neutral)

Global equities saw strong inflows in the final month of the year, and sentiment indicators remain above average. Still, elevated optimism alone does not necessarily signal that the market has reached a significant peak.

Portfolio positioning

We are modestly biased toward stocks over bonds, with a modest preference for U.S. large cap equities and high-quality fixed income.

Macro: Resilient growth, easing inflation amid cooling labor market

The global economy enters 2026 with a backdrop of moderating but resilient growth. The U.S. remains the standout performer, driven by robust capital expenditure, which should continue due to support from full expensing provisions, onshoring initiatives, and transformative investment in artificial intelligence and automation. These factors underpin improved productivity, which help offset demographic headwinds and labor market constraints. Consumer spending should remain healthy, aided by tax refunds and easing financial conditions.

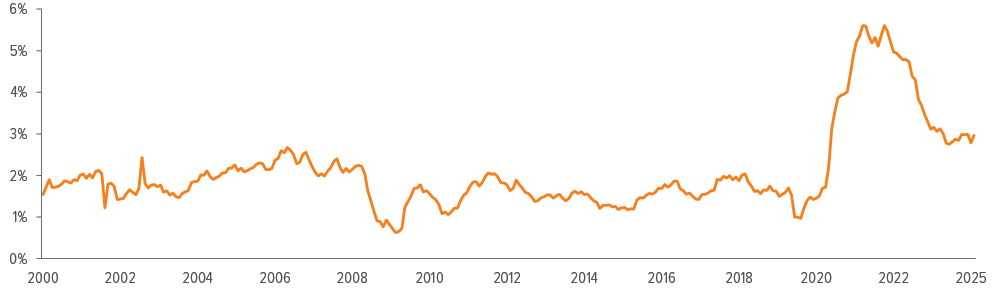

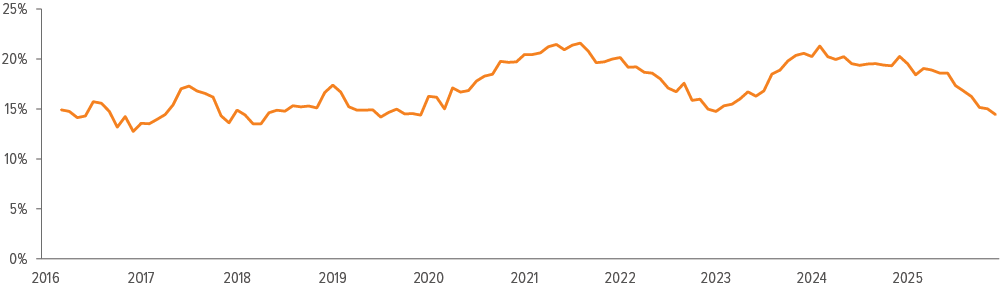

Inflation trends heading into 2026 are broadly constructive. U.S. core inflation is still above the Fed’s target, but it’s moderating (Exhibit 1) as productivity gains from AI adoption and falling shelter costs take hold. Rent and owners’ equivalent rent (OER) are expected to fall through 2026, reducing their contribution to overall price pressures. Meanwhile, tariff-driven goods price increases have been a near-term factor but are expected to fade as supply chains stabilize, paving the way for goods deflation later in the year.

As of 11/30/25. Source: Bloomberg, Voya IM.

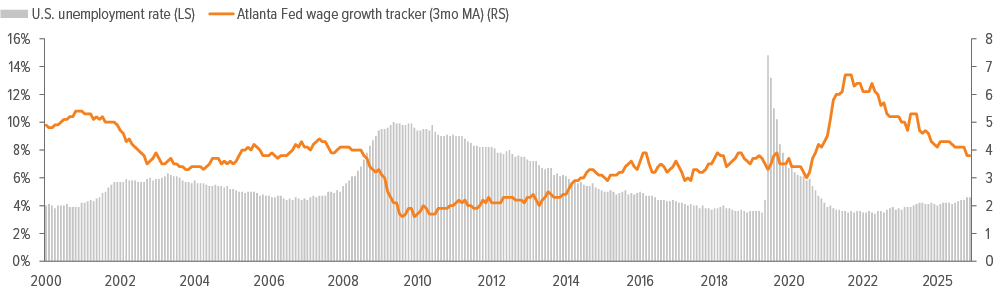

This constructive inflation backdrop should enable the Federal Reserve to maintain a gradual easing cycle aimed at supporting employment. While the U.S. labor market remains on solid footing, signs of cooling are evident: Job growth has slowed, openings and quits have normalized, and the unemployment rate—though still historically low at 4.4%—continues to drift higher from its cycle trough of 3.4% (April 2023). Importantly, this gradual rebalancing has been accompanied by a moderation in wage growth (Exhibit 2), easing inflationary pressure and reinforcing the view of a soft landing rather than a sharp deterioration.

As of 12/31/25. Source: Bloomberg, Voya IM.

U.S. equities are positioned for another year of strength

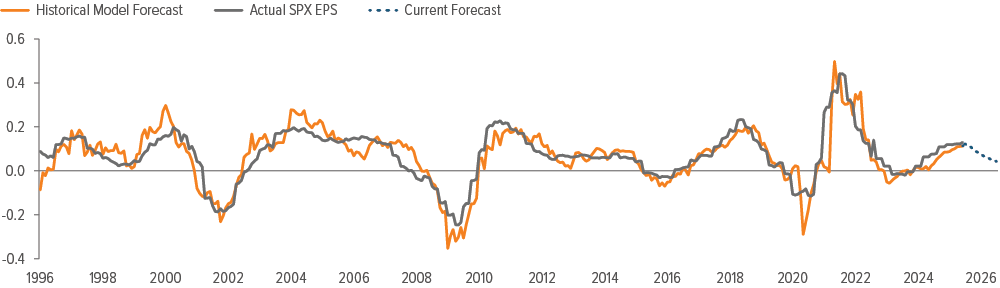

Solid economic growth, lower inflation, and supportive fiscal and monetary impulses should help U.S. equities deliver another year of favorable returns. Large cap stocks remain our portfolio anchor, as they benefit from strong balance sheets, pricing power, and exposure to secular drivers such as artificial intelligence, automation, and digital infrastructure. While earnings growth for large caps is expected to moderate from 2025 highs, it should remain positive (Exhibit 3), led by technology, industrials, and select financials.

As of 12/15/25. Source: Bloomberg, Voya IM.

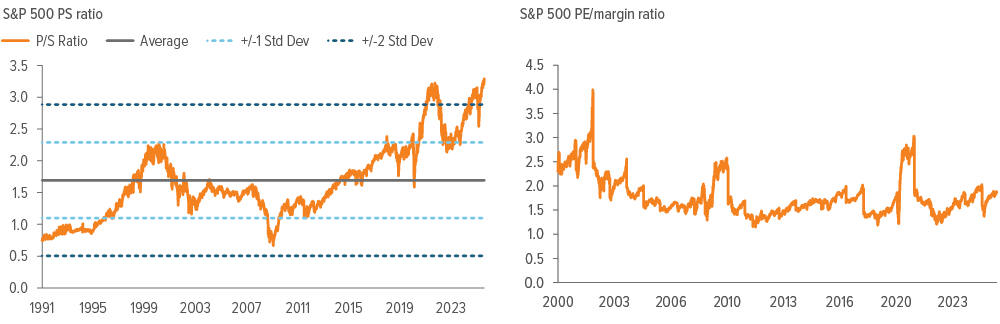

Hyperscalers’ aggressive investment in AI infrastructure and data centers—essential to sustaining innovation—has begun to weigh on free cash flow in the near term (Exhibit 4), even as revenue growth remains robust. This dynamic may contribute to higher volatility, as elevated headline valuations (Exhibit 5, left side) leave markets more exposed to downside growth surprises. However, when we adjust for today’s unusually high margins and exceptional profitability, valuations look more reasonable than they appear at first glance (Exhibit 5, right side), supporting a continued constructive outlook on equities. From a style perspective, we maintain a balanced posture between 1) growth equities driven by innovation and secular trends and 2) value oriented sectors such as financials, industrials, and utilities, which may benefit from normalized economic conditions, increased capital deployment, and regulatory tailwinds.

As of 11/30/25. Source: Bloomberg, Voya IM.

As of 12/15/25. Source: Bloomberg, Voya IM.

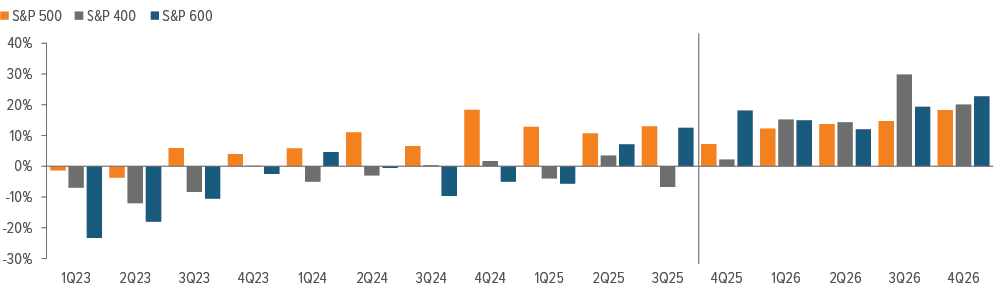

Mid and small cap stocks present a more nuanced picture. Earnings prospects are improving (Exhibit 6) as financial conditions ease and domestic demand firms, offering potential upside for companies with strong innovation pipelines and exposure to reshoring trends. However, higher input costs and less diversified revenue streams are likely to keep volatility elevated, relative to large caps.

As of 01/08/26. Source: Bloomberg, Voya IM.

International equities offer diversification, valuation support, and meaningful global tailwinds

While we prefer U.S. equity fundamentals and connections to mega themes, we remain focused on global diversification, given elevated U.S. valuations and concentration risk, election-related volatility, and compelling structural opportunities abroad.

Europe

Europe continues to face structural challenges that constrain growth prospects. Competitiveness challenges, political fragmentation, and the high costs of energy transition weigh on economic momentum. While GDP growth is expected to remain positive, it should lag the U.S. and other developed peers, reflecting slower industrial output and uneven fiscal responses. Inflation is easing, but disinflation will be gradual, driven primarily by persistent cost pressures—such as energy prices, labor market rigidities, and fiscal measures—rather than demand-driven overheating. These forces are likely to shape the inflation path even as the European Central Bank concludes its rate-cutting cycle.

From an investment perspective, European equities earnings growth is expected to modestly trail the U.S., constrained by slower GDP growth and margin pressures from, among other things, low-cost Chinese exports. Industrials and luxury goods remain bright spots, benefiting from government spending initiatives and strong demand from high-income consumers. Although much of Europe’s strong returns in 2025 came from valuation expansion, it is less expensive than the U.S., supporting the case for high-quality multinationals with global revenue streams.

United Kingdom

The U.K. faces a more challenging backdrop than continental Europe. Elevated mortgage costs, fiscal tightening, and subdued consumer confidence limit domestic demand. Inflation is moderating but remains sticky due to housing and health care costs. Equity market prospects are muted. While some global companies in energy and consumer staples offer stability, broader market performance is likely to lag other developed peers. However, for foreign investors, currency effects could be a contributor, as the sterling may gain on fiscal tightening to stabilize debt dynamics.

Japan

Japan offers relative stability, supported by corporate governance reforms, shareholder-friendly measures, and new leadership signaling pro-growth fiscal and dovish monetary policies. While political uncertainty and inflation remain concerns, policymakers welcome moderate inflation to boost wages and demand after decades of deflation. Rising prices from wage reforms and food costs make this a delicate balance, as excessive inflation could erode purchasing power. As a result, the Bank of Japan is expected to raise rates this year. Longer term, structural shifts toward automation and robotics align with global investment themes, and earnings growth should benefit from export competitiveness and domestic capital expenditure.

Emerging markets: Balancing cyclical headwinds with competitive advantages and regional tailwinds

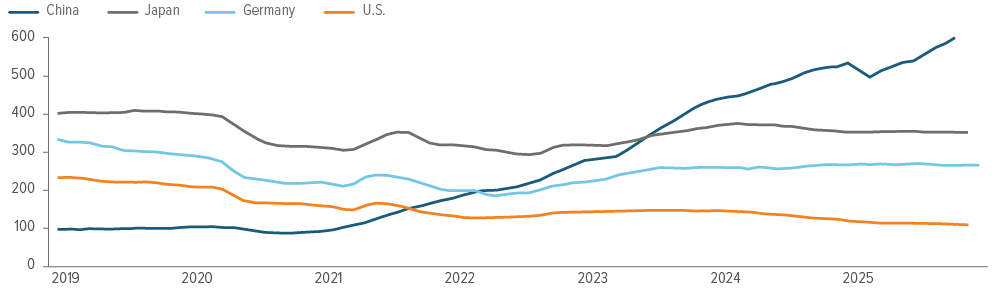

China

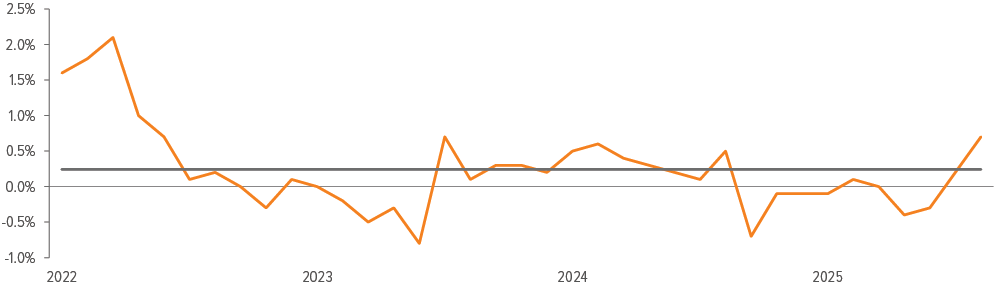

The near-term outlook is mixed. The property sector’s prolonged weakness and fragile consumer confidence continue to weigh on economic momentum, hindering a sustained recovery. These pressures are reflected in prices, with headline inflation near zero (Exhibit 7)—a result of property sector deleveraging, soft household spending, and weak credit demand despite abundant liquidity. Years of policy-driven capital reallocation away from real estate and toward industrial sectors to “de-westernize” supply-chains have further constrained consumption. To offset these pressures, the People’s Bank of China is expected to maintain an accommodative stance, keeping liquidity abundant. However, translating this liquidity into real economic activity will require restoring confidence and addressing structural imbalances.

As of 11/30/25. Source: Bloomberg

At the same time, China’s competitive advantages are hard to ignore. It is the global manufacturing leader producing sophisticated goods at lower costs than most developed markets. For example, China is now the world’s largest automotive exporter (Exhibit 8). Its massive, low-cost electricity generation provides a critical edge for energy-intensive industries and AI infrastructure build-out. A substantial current account surplus creates significant domestic savings, part of which may be deployed in local equities. Recognition of these strengths, coupled with a policy shift to curb inefficient competition and improving equity market sentiment, point to a more constructive outlook.

At the same time, China’s competitive advantages are hard to ignore. It is the global manufacturing leader producing sophisticated goods at lower costs than most developed markets. For example, China is now the world’s largest automotive exporter (Exhibit 8). Its massive, low-cost electricity generation provides a critical edge for energy-intensive industries and AI infrastructure build-out. A substantial current account surplus creates significant domestic savings, part of which may be deployed in local equities. Recognition of these strengths, coupled with a policy shift to curb inefficient competition and improving equity market sentiment, point to a more constructive outlook.

As of 01/26/26. Source: MacroMicro.

Other emerging markets

Performance across other emerging markets is uneven: Commodity-linked economies are supported by stable demand and supply constraints, while others struggle with structural and policy challenges, including weak domestic growth and external vulnerabilities.

India stands out as a structural growth story, supported by strong domestic demand, favorable demographics, and government-led infrastructure investment. Technology services, financials, and consumer sectors are well-positioned to benefit from these trends, and, while valuations are elevated, policy stability and earnings momentum reinforce a positive outlook.

Latin America offers a differentiated opportunity set: Brazil and Chile should benefit from steady demand for energy and metals, while Mexico benefits from nearshoring and tighter integration with U.S. supply chains. Political risk and currency volatility remain headwinds, but exposure to high-quality companies aligned with global trade flows can add diversification. The recent U.S. engagement in Venezuela underscores a renewed focus on Western Hemisphere resource security. While its near-term global economic impact is negligible, this shift could influence regional geopolitics and investment sentiment over time.

Fixed income tilts towards the U.S. anchored by strong credit quality and yield differentials

Core fixed income

Core fixed income fundamentals remain solid, overall. Investment-grade issuers continue to show strong credit profiles, supported by steady revenue and earnings growth (outside commodity sectors), and overall leverage remains contained. While rating downgrades have recently outpaced upgrades and fallen angel risk2 has ticked higher, most large borrowers—particularly those investing heavily in AI—retain strong balance sheets and robust cash flows, limiting near-term credit stress. Market technicals will likely dominate spread behavior as issuances surge to meet refinancing needs, fund M&A, and support technology-driven capital spending. Despite this supply pressure, demand for U.S. bonds should hold up thanks to attractive yields relative to developed market peers. Spreads remain tight, so bouts of volatility could create tactical entry points, with intermediate maturities looking most attractive. In high yield, defaults remain near historical lows, and issuers generally exhibit healthy liquidity and balance sheet strength, though refinancing activity and tighter spreads warrant careful credit selection.

U.S. dollar

The U.S. dollar is expected to weaken gradually in 2026, due to three key factors:

- Monetary policy, which is diverging as the Federal Reserve continues its easing cycle to address labor market vulnerabilities, reducing the dollar’s yield advantage and narrowing rate differentials versus other major currencies.

- Valuation and trade dynamics, with the dollar remaining overvalued on a purchasing power parity basis and persistent U.S. trade deficits exerting structural downward pressure, while global trade stabilization and supply chain diversification strengthen demand for alternative reserve currencies.

- Risk sentiment and the safe-haven role, as improving global growth outside the U.S. and fewer geopolitical shocks limit the flight to quality, though the dollar retains some defensive appeal during periods of volatility.

Commodities: Mixed outlook with range‑bound oil, supportive precious metals, and long‑term industrial demand

Oil

Crude oil prices are expected to remain range-bound in 2026, likely settling in the mid-$50s to $60s per barrel by year-end. This outlook reflects supply and demand dynamics. On the supply side, OPEC+ production discipline is countered by rising U.S. shale output and incremental non-OPEC supply, which are elevating global inventories. Demand growth is muted due to slower global economic activity and subdued industrial output in China, while the accelerating energy transition continues to cap long-term consumption expectations. Geopolitical risks may create short-lived price spikes, but structural oversupply limits the potential for sustained upward price moves.

Precious metals

Gold is positioned for strength in 2026, supported by several factors. A softer U.S. dollar and lower interest rates enhance gold’s appeal as a store of value, while ongoing central bank purchases—particularly from emerging markets—provide a steady demand base. Additionally, gold’s role as a hedge against geopolitical uncertainty and equity market volatility remains intact, making it an attractive allocation in diversified portfolios. Silver may benefit from similar dynamics, with added support from industrial applications tied to renewable energy technologies.

Industrial metals

Base metals such as copper face near-term headwinds from slowing global growth and uneven infrastructure spending, particularly in China. However, structural demand linked to electrification, renewable energy projects, and grid modernization provide a long-term tailwind. While short-term price volatility is likely as markets adjust to cyclical softness, the medium-term outlook remains constructive for metals tied to the global energy transition.