ISM Highlights Diverging Supply and Demand Dynamics

CIO, Multi-Asset Strategies and Solutions

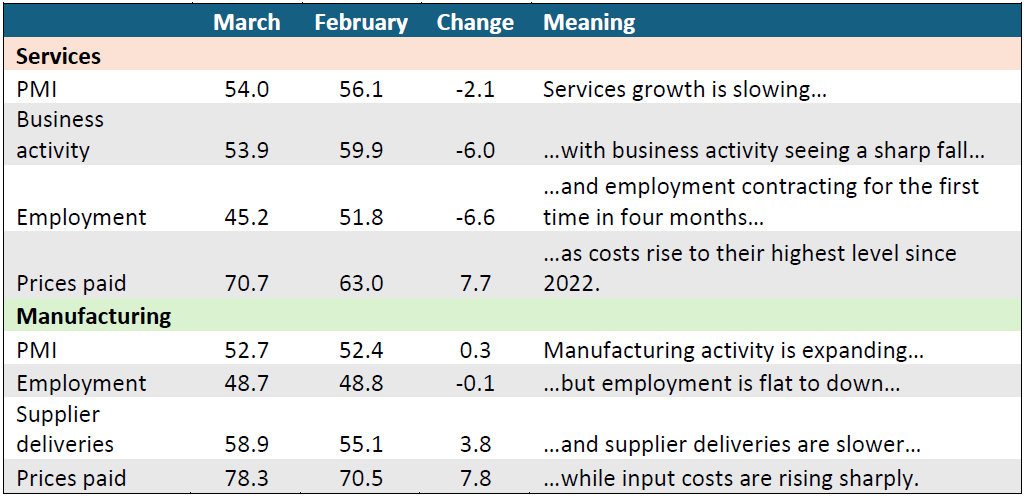

In ISM’s March survey, released this week, Services and Manufacturing remained in expansion territory for a third consecutive month—though the underlying inputs tell different stories. Here’s what’s worrying about these numbers.

As at 04/06/26. Source: ISM. Note that "Supplier deliveries" is a category where higher numbers mean lower deliveries. For all other categories, higher numbers mean expansion or increase.

March represented a full month of conflict with Iran, as well as a renewal of economic policy uncertainty after the Supreme Court struck down U.S. import tariffs imposed under the International Emergency Economic Powers Act in late February.

Services activity cooled meaningfully during the month, driven by the sharpest decline in Business Activity since late 2025 and a significant drop in Employment into contraction. At the same time, the Prices Paid index surged to its highest level since 2022. This divergence reflects rising energy and transportation costs tied to Middle East disruptions, rather than renewed demand strength.

Manufacturing showed a modest headline improvement, but the underlying data suggest the gains were largely supply driven. Slower Supplier Deliveries and a sharp rise in Prices Paid over the past two months have pushed input costs to their highest levels since mid 2022, even as New Orders, Exports, and Employment show signs of softening.

Taken together, the data presents a challenging mix of cooling labor and demand dynamics alongside persistent cost pressures. How much of this is directly attributable to the conflict with Iran and diminished activity due to economic policy uncertainty is difficult to say, but the effects of tariffs and geopolitical conflicts on U.S. economic activity will bear close watching over the coming months.

Julia Rozenfeld contributed to this article.