June liquidity events related to portfolio companies in which PIF invests through its private equity holdings.

Realized distributions turn paper gains into cash that can be redeployed into new investments to drive future returns. Pomona Investment Fund (PIF) is built around this dynamic.

By purchasing fund interests later in their life cycles, PIF focuses on investments with greater visibility into near-term return of capital. As distributions are received, that capital is recycled into new opportunities.

Below, we highlight select recent exit transactions from PIF, illustrating why liquidity matters in private equity investing. (Learn more about the importance of liquidity)

Distributions as a percent of total return1

PIF: 54%

Peer average: 31%

Triton to sell Ramudden Global to I Squared Capital

Funds advised by Triton Partners announced an agreement to sell Ramudden Global to I Squared Capital.

Ramudden Global provides temporary traffic management services that ensure safety compliance for road, utility, and infrastructure works. It operates a network of more than 190 depots across 13 countries in Europe and North America, with over 5,000 highly specialized employees supporting a base of more than 10,000 customers.

Ramudden Global was created by Triton, together with its founders and management, through the acquisition of several individual platform companies beginning in 2017 with Ramudden (Sweden), and in 2018 with AVS (DACH), Chevron (UK), and Fero (Benelux). The individual companies merged into one group in 2020, growing from a European market player into a pan-Atlantic platform with the addition of Canada-based RSG International in 2024 and U.S.-based Curtin in 2025. The joint group turnover as of January 2026 is more than €1 billion (USD $1.2 billion).

The sale highlights Triton’s repeatable buy-and-build playbook, combined with its hands-on operational value-creation capabilities. During Triton’s ownership, Ramudden Global has completed more than 66 add-on acquisitions, expanding into adjacent geographies and rolling out market-leading digital technology across the group.

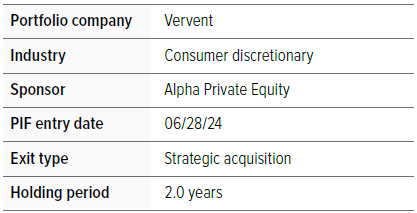

Proskauer advises Alpha Private Equity on signing of agreement for sale of VerVent Audio Holding to Barco

Proskauer advised the VerVent Group and its majority shareholder, Alpha Private Equity, in connection with signing an agreement for the sale of 100% of the share capital of VerVent Audio Group, a French‑British company specializing in high‑end audio, to Barco, a global technology group headquartered in Courtrai (Kortrijk), Belgium.

This transaction marks a successful exit for Alpha and represents a strategic step for Barco, which is expanding its capabilities in high‑end audio and strengthening its position as a provider of integrated audiovisual solutions.

Based in Saint‑Étienne, VerVent is a group specializing in premium audio with a recognized heritage in designing and manufacturing high‑end audio systems under its globally renowned brands Focal and Naim. The group offers a broad portfolio including premium loudspeakers, immersive and active audio solutions, headphones, studio monitors, and OEM automotive audio systems, complemented by a growing offering of bespoke installations and home‑cinema solutions.

Alpha partnered with VerVent to support its transformation into a global reference platform in premium audio and to accelerate its international development. During the investment period, Alpha worked closely with the management team to strengthen the company’s strategic positioning, expand its global footprint, and enhance its operational capabilities.

H.I.G. Capital completes sale of Celerion, highlighting a period of robust exit activity

H.I.G. Capital, a global alternative investment firm with $75 billion of capital under management, announced the completion of the sale of Celerion Holdings, Inc. to funds affiliated with THL Partners for $1.8 billion. Celerion is a global contract research organization focused on clinical pharmacology.

The transaction marks the latest in a series of successful exits from H.I.G.’s Advantage strategy, which has now completed the sales of St. Croix, United Flow Technologies, and Celerion since the fourth quarter of 2025, for a combined total enterprise value of more than $4.5 billion. These transactions underscore H.I.G.’s consistent ability to identify differentiated businesses, execute disciplined value creation strategies, and deliver compelling returns for its investors.

H.I.G. Advantage invests in established, high-quality, industry-leading North American companies with clear and differentiated value propositions. The strategy has demonstrated a consistent ability to identify and build businesses of scale across sectors and geographies.

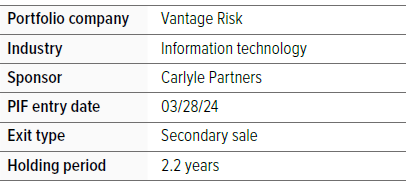

Vantage Group Holdings to be acquired by Howard Hughes Holdings

Vantage Group Holdings Ltd., a privately held specialty insurance and reinsurance company backed by Carlyle and Hellman & Friedman, completed an agreement for Howard Hughes Holdings Inc. to acquire 100% of Vantage for $2.1 billion in cash, or approximately 1.5x year-end 2025 book value. The transaction anchored Howard Hughes’ transformation into a diversified holding company.

Founded in 2020, Vantage has scaled into a next-generation leading specialty insurer and reinsurer, offering a diversified portfolio of global P&C products supported by modern infrastructure and advanced analytics.

Vantage will continue to operate with the same name, brand, and culture, with colleagues retaining the same roles, teams, and go-to-market strategy. HHH’s holding-company ownership of Vantage provides long-term capital support which materially strengthens Vantage’s credit profile and underwriting flexibility. An emphasis on underwriting profitability—driven by disciplined risk selection, pricing, and portfolio optimization rather than growth—will allow Vantage to effectively navigate the insurance cycle and optimize asset allocation over time.

Cinven, KKR and Providence sell stake in MasOrange for €4.25 billion

Cinven, KKR, and Providence, the sponsors of Lorca JVCo (“Lorca”), the entity through which they indirectly own 50% of MasOrange, completed the sale of their remaining stake to Orange. The transaction represents a significant milestone for Spain’s telecommunications operator. Under the terms of the agreement, Lorca received total cash proceeds of €4.25 billion.

In 2020, the trio strategically partnered with management and local shareholders to facilitate the €5.3 billion take-private of MásMóvil. MasOrange was formed in 2024 by the merger of MásMóvil and Orange España, with Orange Group owning 50% of the combined group and Lorca the remaining half. At the time of the take-private, MásMóvil was the fourth-largest player in the Spanish telecoms market with more than 11 million customers. Under the consortium’s ownership, MasOrange has developed into the telecommunications operator with the highest number of subscribers in Spain, serving over 33 million lines. The sponsors have partnered closely with management to organically grow the business, develop a top-quality product offering and customer satisfaction, as well as reduce churn. Over the course of the sponsors’ investment, MásMóvil also completed more than 10 network transactions and 7 accretive acquisitions, including the transformative take-private of Euskaltel in 2021 and the merger with Orange España in 2024. Earlier this year, MasOrange also created one of the largest independent fiber networks in Europe by merging its network assets with those of Vodafone Spain.

Types of liquidity events

- Continuation vehicle: A PE firm extends its holding period in a portfolio company through a new fund.

- IPO: A privately held company lists on a public exchange, converting the PE firm’s stake into publicly traded shares

- Recapitalization: A portfolio company issues debt to pay a dividend to the PE firm, generating returns prior to exit.

- Secondary sale: A PE firm sells its stake in a company to another PE firm.

- Strategic acquisition: Another company acquires the portfolio company, typically at a premium that reflects its strategic value.

Risk of investing Discussed below are the investments generally made by Investment Funds and the principal risks that the Adviser and the Fund believe are associated with those investments and with direct investments in operating companies. These risks will, in turn, have an effect on the Fund. In response to adverse market, economic or political conditions, the Fund may invest in investment grade fixed income securities, money market instruments and affiliated or unaffiliated money market funds or may hold cash or cash equivalents for liquidity or defensive purposes, pending investment in longer-term opportunities. In addition, the Fund may also make these types of investments pending the investment of assets in Investment Funds and Co-Investment Opportunities or to maintain the liquidity necessary to effect repurchases of Shares. When the Fund takes a defensive position or otherwise makes these types of investments, it may not achieve its investment objective. The value of the Fund’s total net assets is expected to fluctuate in response to fluctuations in the value of the Investment Funds, direct investments and other assets in which the Fund invests. An investment in the Fund involves a high degree of risk, including the risk that the Shareholder’s entire investment may be lost. The Fund’s performance depends upon the Adviser’s selection of Investment Funds and direct investments in operating companies, the allocation of offering proceeds thereto, and the performance of the Investment Funds, direct investments, and other assets. The Investment Funds’ investment activities and investments in operating companies involve the risks associated with private equity investments generally. Risks include adverse changes in national or international economic conditions, adverse local market conditions, the financial conditions of portfolio companies, changes in the availability or terms of financing, changes in interest rates, exchange rates, corporate tax rates and other operating expenses, environmental laws and regulations, and other governmental rules and fiscal policies, energy prices, changes in the relative popularity of certain industries or the availability of purchasers to acquire companies, and dependence on cash flow, as well as acts of God, uninsurable losses, war, terrorism, earthquakes, hurricanes or floods and other factors which are beyond the control of the Fund or the Investment Funds. Unexpected volatility or lack of liquidity, such as the general market conditions that prevailed in 2008, could impair the Fund’s performance and result in its suffering losses. The value of the Fund’s total net assets is expected to fluctuate. To the extent that the Fund’s portfolio is concentrated in securities of a single issuer or issuers in a single sector, the investment risk may be increased. The Fund’s or an Investment Fund’s use of leverage is likely to cause the Fund’s average net assets to appreciate or depreciate at a greater rate than if leverage were not used. The Fund is a non-diversified, closed-end management investment company with limited performance history that a Shareholder can use to evaluate the Fund’s investment performance. The Fund may be unable to raise substantial capital, which could result in the Fund being unable to structure its investment portfolio as anticipated, and the returns achieved on these investments may be reduced as a result of allocating all of the Fund’s expenses over a smaller asset base. The initial operating expenses for a new fund, including start-up costs, which may be significant, may be higher than the expenses of an established fund. The Investment Funds may, in some cases, be newly organized with limited operating histories upon which to evaluate their performance. As such, the ability of the Adviser to evaluate past performance or to validate the investment strategies of such Investment Funds will be limited. In addition, the Adviser has not previously managed the assets of a closed-end registered investment company. Closed-End Fund; Liquidity Risks. The Fund is a non-diversified closed-end management investment company designed principally for long-term investors and is not intended to be a trading vehicle. An investor should not invest in the Fund if the investor needs a liquid investment. Closed-end funds differ from open-end management investment companies (commonly known as mutual funds) in that investors in a closed-end fund do not have the right to redeem their shares on a daily basis at a price based on net asset value. |