Key Takeaways

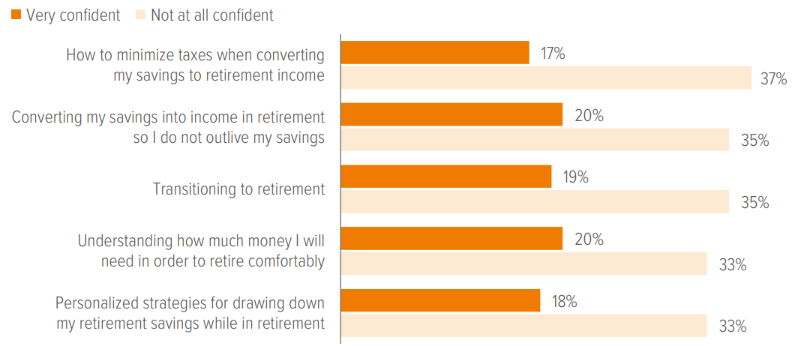

Participants approaching retirement are asking for help with retirement income planning—and their confidence in this area is low, particularly where the decisions are hardest.

A retirement tier is the set of investment solutions within a DC plan designed to help participants convert savings into sustainable income.

We offer a four-part approach for sponsors and DC specialists who want to close the gap between what their plan promises and what it delivers, with particular attention to the DC specialist’s role in the retirement income conversation.

DC plans are designed for accumulation. The retirement tier—the part of the plan designed to help participants convert savings into income—is where most plans have more to offer than sponsors realize.

As workers approach retirement, their priorities shift. Am I saving enough? becomes Will this last?

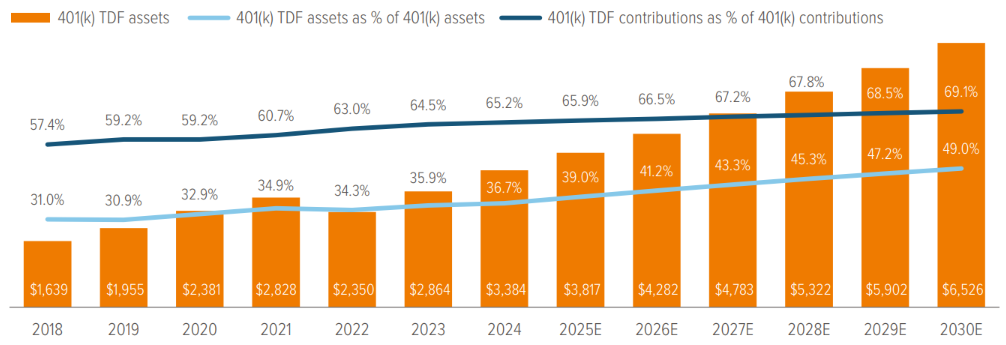

For most participants, both questions have the same starting point: a target date fund (TDF). TDF assets now represent an estimated 39% of all DC plan assets, up from 31% in 2018; Cerulli projects they’ll account for nearly half by the end of the decade. Contributions flowing into TDFs as a share of total 401(k) contributions now exceed 65%. The TDF is how most participants save for retirement. What happens when it’s time to spend is a question the industry hasn’t fully answered—and participants know it.

Source: Department of Labor, Investment Company Institute, PSCA, Vanguard “How America Saves,” and Cerulli Associates, U.S. Defined Contribution Distribution 2025.

Voya’s research finds that participant confidence in making retirement income decisions remains low—and lowest precisely where the stakes are highest: converting savings into income, understanding how long assets will last, and building a drawdown strategy.

As of 04/01/25. Source: Voya IM, 2025 Survey of the Retirement Landscape.

DC specialists may have more influence here than they realize. Nearly two-thirds of active participants have no financial advisor. Half say they plan to find one as they approach retirement.1 Until then, they report their plan sponsor as their primary source of financial guidance; for many, it’s the most consistent financial relationship they have.

A note about risk: There is no guarantee that any investment option will achieve its stated objective. Principal value fluctuates and there is no guarantee of value at any time, including the target date. The “target date” is the approximate date when an investor plans to start withdrawing their money. When their target date is reached, they may have more or less than the original amount invested. Stocks are more volatile than bonds, and portfolios with a higher concentration of stocks are more likely to experience greater fluctuations in value than portfolios with a higher concentration in bonds. Foreign stocks and small- and mid-cap stocks may be more volatile than large-cap stocks. Investing in bonds also, entails credit risk and interest rate risk. Generally, investors with longer timeframes can consider assuming more risk in their investment portfolio. Guarantees are based on the claims-paying ability of the insuring company.