Most advisors building a DC practice spend their energy on the obvious levers: plan design, investment menu, fee benchmarking. Caregiver support is just as real, and rarely shows up on a plan review.

The Americans with Disabilities Act, whose anniversary falls this month, rebuilt the physical workplace around access. The financial side of disability never got the same attention.

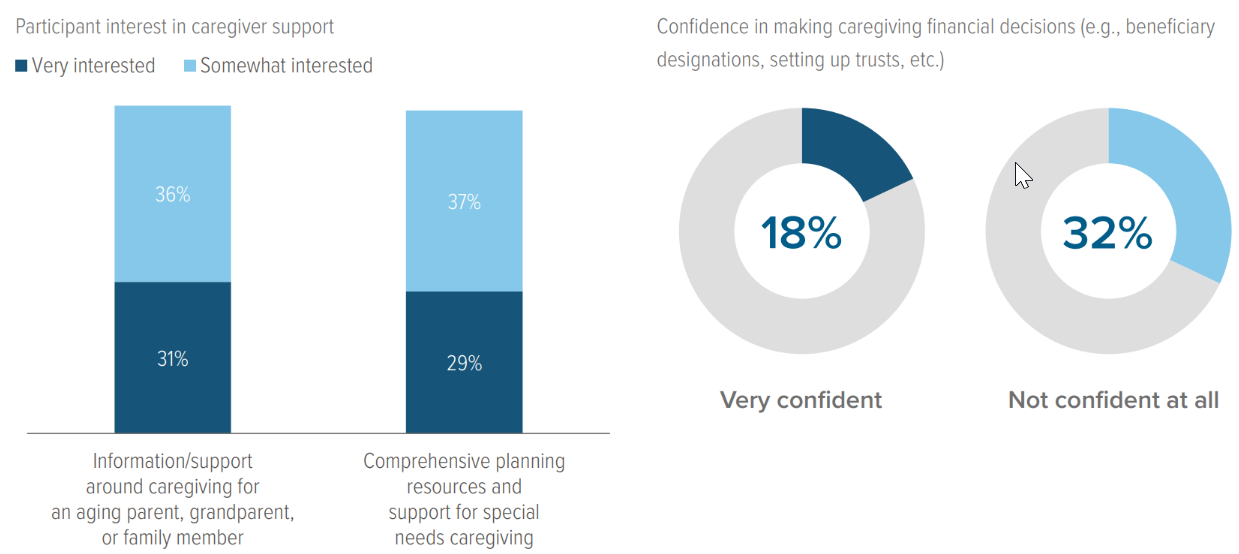

Voya IM’s most recent Survey of the Retirement Landscape: Participant Perspectives found that 15% of participants identified as caregivers, and another 5% reported a disability or special needs of their own. Two-thirds said they were very or somewhat interested in comprehensive planning resources aimed at caregivers.

DC plan sponsors have consistently underestimated how much caregiving their participants are doing, even as they name caregiver financial needs a priority for the next two years. So the demand goes unmet.

As of 04/01/25. Source: Voya IM.

A workforce issue dressed up as a benefits question

Caregiving follows people to work. The participant managing a parent’s care, or planning around a child who will need lifelong support, carries that weight into every retirement decision. It shapes how much they save, when they think they can stop working, and what they expect to do with their assets once they get there.

About a third of participants told Voya they weren’t sure what they’d do with their retirement assets after retiring, and that uncertainty runs deepest among the people managing complications the standard planning conversation ignores. The math is worse for them, and they know it. In a separate Voya survey, 49% of caregivers said their responsibilities have had a severe or major impact on their ability to prepare for retirement. A caregiver isn’t weighing whether to pick the 2045 target date fund; they’re asking whether they can retire at all without leaving someone they love exposed.

Standard financial wellness content doesn’t answer that. Government benefit eligibility, special needs trusts, the mechanics of who gets named on a form— most participants have no idea where to start. Our survey says they want help, but few are being offered any.

The mistake an advisor can catch that a participant never sees

A parent enrolls in benefits at a new job and names their child with a disability as beneficiary. It’s a reasonable instinct—and a costly one. Because SSI and Medicaid are means-tested, an inheritance of as little as $2,000 can disqualify that child from the benefits they rely on.

The fix could be a special needs trust named as beneficiary instead, so the assets pass without touching eligibility. A participant clicking through a beneficiary form online will almost never catch this. A well-prepared advisor will.

Multiply that across a plan and the case for a DC specialist stops being abstract. Participants working with an advisor were 25% more likely to feel prepared for retirement than those without. Extend that guidance into caregiving. Most DC specialists are underestimating this demand, the same as sponsors. Be the one who doesn’t, and you’re solving a problem the competition hasn’t noticed.

Voya Cares® has your back

The finals presentation changes when you walk in with client-ready material instead of good intentions. Voya Cares® supplies it: a planning checklist that runs from guardianship to beneficiary review to trust decisions, a government benefits roadmap covering SSI, SSDI, Medicaid, and Medicare, and case studies on the income gap, beneficiary designations, and special needs trusts you can hand a prospect to open the conversation.

For the plan sponsor, this is retention: support in the areas employees actually care about gives them a reason to stay. For the DC specialist, it’s a way into a plan that has nothing to do with shaving another basis point off the fee.

Two DC specialists walk into the same finals. One brings a fund lineup and competes on price. The other does the same but also brings a caregiver strategy and the materials to back it. Which one do you think the sponsor remembers?