Strong plan metrics don’t always reflect how participants feel. Research shows confidence gaps that can remain hidden in plain sight.

Most retirement plans appear healthy when evaluated using traditional metrics. Participation rates, average deferrals, and account balances often suggest steady progress toward retirement readiness.

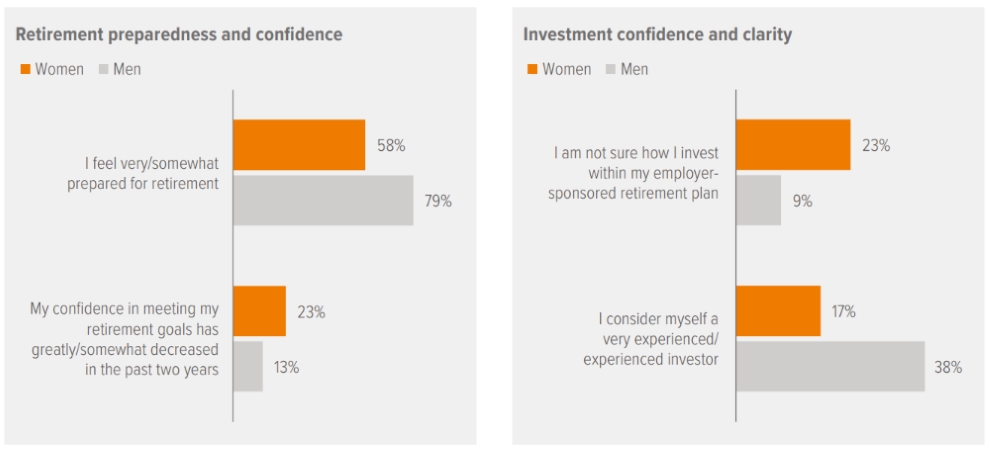

Research from our most recent Survey of the Retirement Landscape, however, shows that readiness is not experienced evenly across the workforce. One of the most persistent differences appears along gender lines. Women are significantly less likely than men to say they feel prepared for retirement and more likely to report declining confidence, limited investing experience, and uncertainty about how their retirement plan assets are invested. This confidence gap shows up consistently across market environments and tends to widen as retirement approaches.

Women’s History Month provides a timely opportunity to surface this issue. Framed appropriately, the conversation is not about targeting a specific group, but about understanding whether the plan supports a diverse workforce with different needs, responsibilities, and decision-making styles.

These differences show up not only in how prepared participants feel, but also in how confident and informed they are when making investment decisions within their employer sponsored retirement plan.

As of January 2025. Source: Voya, 2025 Survey of the Retirement Landscape: Participant Perspectives.

When readiness is assessed only at the plan level, these differences in confidence, experience, and decision clarity can be difficult to detect. Aggregate metrics smooth out differences in participant experience, making it possible for meaningful confidence gaps to persist without drawing attention.

Confidence matters because it influences behavior. Participants who feel uncertain or inexperienced are more likely to disengage from plan communications, delay retirement decisions, or avoid making changes until choices become urgent. Over time, this can affect workforce planning, retirement timing, and overall satisfaction with benefits.

Research also points to factors associated with narrower confidence gaps. Participants with access to advice, simplified investment options, and clear defaults are more likely to report feeling prepared for retirement. Confidence appears to reflect not only savings behavior, but the degree to which participants feel informed and supported when making decisions about their plan.

Expanding how readiness is discussed allows sponsors to move beyond averages and focus on participant experience. That shift makes it easier to identify where communication, plan design, or access to guidance may be contributing to uneven outcomes, even in otherwise well run plans.

What advisors can do

Sponsoring client events that focus on decision clarity, life context, and small, achievable actions can help participants build confidence without singling out any group.

Formats such as open Q&A sessions, life-stage workshops, and plain English plan walkthroughs are especially effective for participants who may feel uncertain or inexperienced—a dynamic that our research shows is more common among women.