AI Was the Rising Tide That Lifted All Boats—Until It Wasn’t

Chief Investment Officer, Equities

Senior Portfolio Manager, Large/Mid Cap Growth Equities

Client Portfolio Manager, Large and Mid Cap Growth Equities and Systematic Equities

Key Takeaways

Artificial intelligence (AI) has entered a new era—one that rewards knowing where to be, not just whether to be there.

Most AI spending is responding to real, existing demand, but not all of it carries the same risk or return profile.

As dispersion rises, active judgment outweighs blanket exposure.

For a time, simply being exposed to AI drove returns. That phase is over. AI investment has scaled to a level that is reshaping markets, business models, and outcomes—rewarding selectivity over blanket exposure as companies begin to diverge.

Download Advisor Brief Download Client-Approved Summary

Artificial intelligence has moved from concept to capital. What began as a future-oriented theme is now reshaping investment flows, corporate strategy, and the real economy in real time.

In the early stages of this cycle, the experience was relatively straightforward. Expectations rose together, participation was broad, and most investors benefited. Large technology platforms led the way, infrastructure demand surged, and AI exposure itself became the primary driver of returns.

Momentum defined that phase. It rewarded proximity to the theme rather than precision within it.

Today, the landscape looks different. AI investment has scaled materially, volatility has increased, and leadership has begun to shift. Markets are no longer treating AI as a single, monolithic opportunity. Instead, they are differentiating between business models, end markets, and degrees of exposure. What once resembled a rising tide lifting nearly all boats has given way to a more uneven environment where outcomes diverge meaningfully.

This transition is not a signal that the AI opportunity has faded, but that the easy part is behind us.

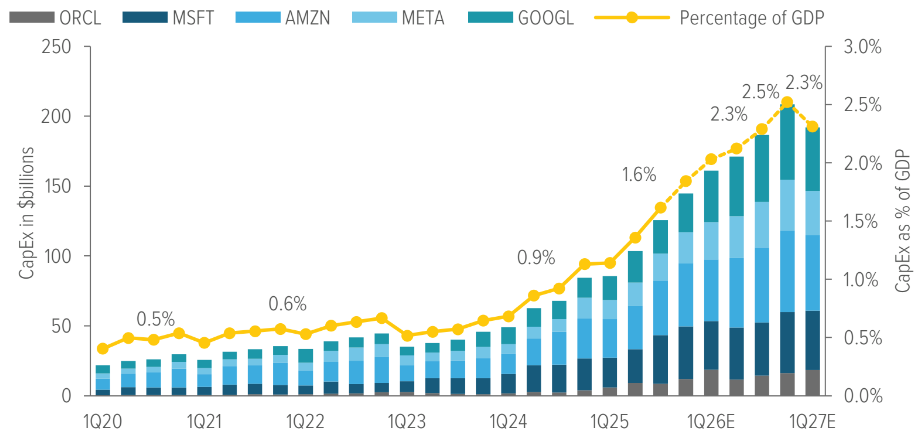

The scale of AI investment

Much of the current debate around AI centers on the magnitude of capital spending. That focus is warranted. AI-related investment by hyperscalers has reached a scale that is no longer incremental. It now represents a significant share of U.S. economic activity, placing it alongside other historically important technological inflection points (Exhibit 1).

As of 03/31/26. Source: Company filings, Visible Alpha, FRED.

At this level, AI investment begins to influence more than earnings growth for a handful of companies. It affects capital allocation across industries, labor demand, energy infrastructure, and supply chains. It also invites scrutiny. Investors have seen periods before when enthusiasm for transformative technology drove capital spending faster than eventual returns could justify.

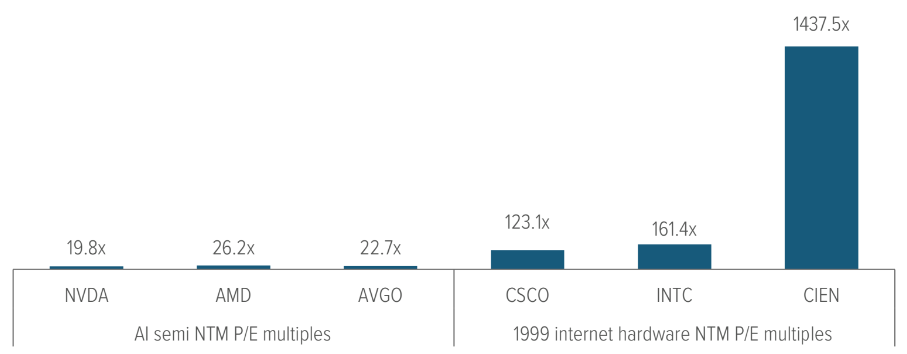

Unsurprisingly, comparisons to the late-1990s internet buildout have resurfaced. Valuation concerns have followed. Semiconductors, the most visible beneficiaries of the AI buildout to date, are often cited as examples of excess. In isolation, some multiples appear elevated (Exhibit 2).

Context changes the picture. Current valuations remain well below the extremes reached during the peak of the internet hardware bubble. More importantly, valuation alone does not determine whether capital spending is productive. The more relevant question isn’t how much is being spent, but why–and where the economic benefits are likely to accrue.

As of 03/31/26. Source: Bloomberg consensus estimates.

Demand visibility: Spending that follows usage, not hope

One of the most important distinctions between the current AI cycle and earlier technology booms is demand visibility. In prior periods, infrastructure investment often preceded usage by years. Companies deployed capital in anticipation of adoption that had yet to materialize, leaving investors exposed to long gaps between spending and economic payoff.

Today, much of the AI buildout is responding to observable demand rather than speculative expectation. Hyperscalers continue to report strong utilization across cloud, compute, and AI-enabled services, with management commentary consistently pointing to capacity constraints rather than demand shortfalls. In other words, the limiting factor has been supply, not interest.

Recent results from leading semiconductor and infrastructure providers reinforce this dynamic. Growth has been driven by workloads that already exist, not merely projected use cases. Power availability and grid limitations have emerged as tangible bottlenecks, underscoring the reality that enterprises are actively investing to support current operations rather than future possibilities.

This is notable because it reshapes the risk profile of AI investment. When spending follows usage, uncertainty shifts away from whether demand will arrive and toward how efficiently that demand can be served and monetized. The question becomes one of execution, scalability, and margin durability rather than adoption itself.

That does not eliminate risk, but it changes its character. AI investment is no longer primarily a bet on technological acceptance. It has become a test of which companies can translate visible demand into sustainable economics as capacity expands and competition intensifies. This is a genuine departure from earlier cycles—and a key reason outcomes are beginning to diverge.

Where the money is going, and why it matters

Equally important to the scale of AI investment is how that capital is being allocated. Not all AI spending is pursuing the same objective, and not all of it carries the same economic risk. A significant portion of current investment is directed toward economically grounded use cases—enterprise AI services, core cloud infrastructure , data centers, networking, and platform support tied to identifiable customers and near-term demand. In these areas, spending is responding to workloads that already exist, with clearer visibility into utilization and monetization.

At the same time, a smaller share of capital is flowing into more speculative areas, such as frontier model development and longer-dated research initiatives. These investments may ultimately prove transformative , but their economic payoff is less certain and more distant . Returns depend not only on technical progress, but on future adoption patterns, pricing power, and evolving competitive dynamics that are harder to forecast today.

That gap introduces dispersion. Companies exposed primarily to current, enterprise-driven demand face a different risk-reward profile than those whose fortunes depend on future breakthroughs or shifting monetization models. When capital is tied to observable usage, uncertainty centers on execution and efficiency. When it is tied to longer-dated innovation, uncertainty expands to timing, scale, and capture of value.

As the AI ecosystem matures, markets have grown more sensitive to these differences. Broad participation was rewarded when spending itself was the story. Where capital is deployed—and how directly it translates into sustainable cash flows—is what drives outcomes as allocation differentiates. That is why selectivity is rising; not because AI investment is slowing, but because its economic pathways are diverging

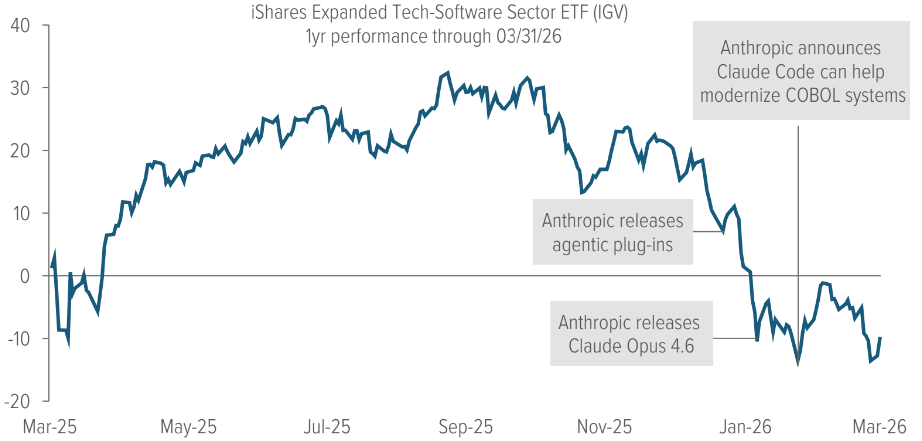

Software disruption and the market’s first overcorrection

As AI capabilities have advanced, investor concern has since moved downstream, particularly into software. What began as a debate about infrastructure spending and compute intensity quickly evolved into a broader fear that AI might not just enhance software workflows, but replace them altogether.

That concern culminated in what many market participants came to describe as a “SaaSpocalypse,” a rapid and largely indiscriminate repricing of application software as fears of AI-driven displacement escalated. A series of high-profile developments, particularly around agentic tools capable of executing tasks autonomously, accelerated this narrative. The implication was stark: if AI could perform work directly, large portions of the software stack might be rendered obsolete.

The market reaction was swift (Exhibit 3). Software sold off sharply, with little differentiation across business models, customer bases, or competitive positioning. The market grouped companies with vastly different economic profiles and repriced them as though the threat were uniform and immediate.

As of 03/31/26. Source: Factset.

That response captured uncertainty, but it lacked nuance.

Some software models are clearly more exposed than others. Products that rely heavily on user-interface workflows, light data moats, or narrow feature differentiation face genuine pressure as AI lowers switching costs and makes functionality easier to replicate, bundle, or build internally. In these cases, AI does not need to eliminate demand entirely to compress margins or weaken pricing power.

At the same time, treating software as a single category at risk obscures important distinctions within the ecosystem. Infrastructure -oriented software plays a fundamentally different role. Tools embedded in cloud modernization, data management, security, networking, and system integration become more critical as AI workloads expand and complexity increases. Scale, reliability, performance, and trust become more important—not less— when AI is deployed at enterprise scale.

From this perspective, the SaaSpocalypse looks less like a verdict on software and more like the market’s first broad overcorrection. AI is not eliminating software value; it is relocating defensibility, shifting competitive advantage away from surface -level features and toward deeper integration, mission-critical functionality, and durable economic moats.

As with earlier stages of the AI cycle, the key takeaway is not that disruption should be ignored, but that differentiation matters. The challenge for investors is no longer identifying whether AI changes the software landscape, but understanding how it does—and which business models are positioned to endure as that change unfolds

From broad exposure to deliberate positioning

AI’s evolution has moved markets from shared optimism to sharper differentiation. In the early stages of the cycle, participation mattered more than precision. Exposure to the theme itself was often enough to drive returns as expectations rose together and leadership remained concentrated.

That environment has changed. As AI investment has scaled and its effects have begun to ripple across industries, outcomes have diverged. The stress tests are no longer uniform across business models. Markets are separating companies positioned to absorb disruption from those exposed to it. This shift does not mark the end of the AI opportunity, but a transition from blanket exposure to purposeful selection.

Enterprise demand for AI-enabled services remains clear, particularly across infrastructure, compute, and core platforms. At the same time, dispersion across business models is increasing. Some companies are seeing their moats reinforced as complexity rises, while others face pressure as AI lowers barriers and accelerates substitution. In this environment, simply being “in AI” is no longer a sufficient differentiator.

Position, not participation, is what drives outcomes now. Selectivity and active judgment take precedence over participation alone. The market’s recent volatility reflects this process of sorting, not a reversal of the underlying trend.

As the easy phase of the AI cycle recedes, the boats best designed to navigate open water become easier to identify—but doing so takes work. It requires understanding where demand proves resilient, where defensibility is shifting, and where the economics of AI adoption are most likely to persist. That is precisely what active management is built for—and where the opportunity of the next stage lies.

A note about risk: The principal risks are generally those attributable to investing in stocks and related derivative instruments. Holdings are subject to market, issuer, and other risks, and their values may fluctuate. Market risk is the risk that securities or other instruments may decline in value due to factors affecting the securities markets or particular industries. Issuer risk is the risk that the value of a security or instrument may decline for reasons specific to the issuer, such as changes in its financial condition. Smaller companies may be more susceptible to price swings than larger companies, as they typically have fewer resources and more limited products, and many are dependent on a few key managers. Artificial intelligence (AI) may pose inherent risks, including but not limited to: issues with data privacy, intellectual property, consumer protection, and anti-discrimination laws; ethics and transparency concerns; information security issues; the potential for unfair bias and discrimination; quality and accuracy of inputs and outputs; technical failures and potential misuse. Users of AI- based technology and tools should take these risks into consideration prior to use of the technology. From broad exposure to deliberate positioning AI’s evolution has moved markets from shared optimism to sharper differentiation. In the early stages of the cycle, participation mattered more than precision. Exposure to the theme itself was often enough to drive returns as expectations rose together and leadership remained concentrated. That environment has changed. As AI investment has scaled and its effects have begun to ripple across industries, outcomes have diverged. The stress tests are no longer uniform across business models. Markets are separating companies positioned to absorb disruption from those exposed to it. This shift does not mark the end of the AI opportunity, but a transition from blanket exposure to purposeful selection. Enterprise demand for AI-enabled services remains clear, particularly across infrastructure, compute, and core platforms. At the same time, dispersion across business models is increasing. Some companies are seeing their moats reinforced as complexity rises, while others face pressure as AI lowers barriers and accelerates substitution. In this environment, simply being “in AI” is no longer a sufficient differentiator. Position, not participation, is what drives outcomes now. Selectivity and active judgment take precedence over participation alone. The market’s recent volatility reflects this process of sorting, not a reversal of the underlying trend. As the easy phase of the AI cycle recedes, the boats best designed to navigate open water become easier to identify—but doing so takes work. It requires understanding where demand proves resilient, where defensibility is shifting, and where the economics of AI adoption are most likely to persist. That is precisely what active management is built for—and where the opportunity of the next.