Financial Literacy Month may be more effective when DC plans simplify participant decisions. What role can DC specialists play in helping sponsors see that?

Every April, many defined contribution (DC) plans roll out Financial Literacy Month programming. Sponsors offer more information, tools, and reminders to engage. They operate on a familiar assumption: if participants understand more, they will feel better prepared.

DC specialists often see a different reality. Even in plans with strong participation and healthier savings rates, participant confidence still lags. Participants don’t disengage because they don’t care, but because decisions feel complex, unclear, or high‑stakes.

This gap highlights what Financial Literacy Month often overlooks. Knowledge isn’t always the constraint. Decision comfort is.

Confidence reflects how plans actually work for participants

Many sponsors treat confidence as a soft or subjective concept. In practice, confidence reflects how participants experience the plan day to day.

Voya’s research shows that participants who report higher confidence also tend to:

- Believe they will reach their retirement goals

- Feel more comfortable with the investment decisions they’ve made

- Experience less stress when they think about retirement

Those differences matter—and they don’t emerge simply because participants know more or engage more often. Plan structure plays a far greater role.

When responsibility outpaces confidence

Across the broader retirement landscape, the same pattern appears repeatedly. Participants shoulder more responsibility for retirement outcomes, yet many lack confidence in their investing ability—particularly as retirement approaches.

They worry about:

- Turning savings into income

- Market downturns at the wrong moment

- Making decisions they can’t reverse

Education alone rarely resolves that tension. In many cases, it intensifies it by adding choices without reducing risk perception.

What can help is clarity.

Simplification can change outcomes

Participants consistently report higher confidence when decisions are simplified and when the plan structure does more of the work on their behalf. Professionally managed solutions designed around retirement goals—such as target date funds (TDFs)— are a clear example.

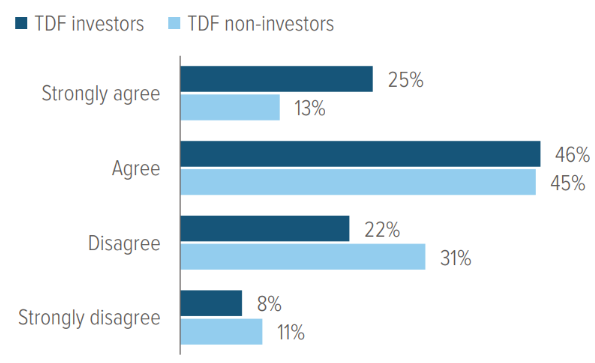

Participants who invested in TDFs are more likely to say they feel confident they would reach their retirement goals (Exhibit 1). Seventy‑one percent of TDF investors agree or strongly agree they are confident, compared with 58% of non‑investors. At the “strongly agree” level, the gap is just as striking: 25% versus 13%.

As of April 2025. Source: Voya IM.

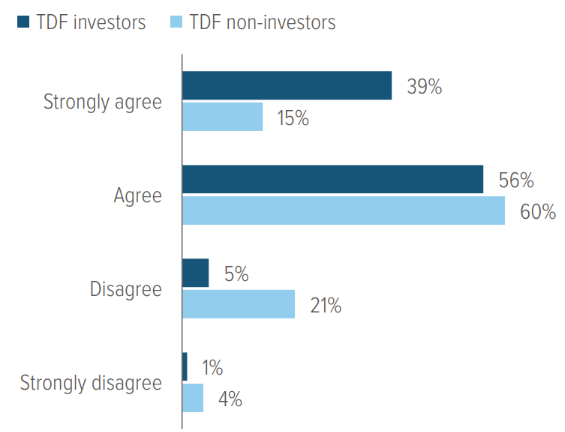

This confidence extends beyond a single question. When asked whether investing in TDFs increased confidence in making good investment decisions, 95% of TDF investors agreed, with 39% strongly agreeing (Exhibit 2). Among participants who do not invest in TDFs, total agreement drops to 75%, with just 15% strongly agreeing.

As of April 2025. Source: Voya IM.

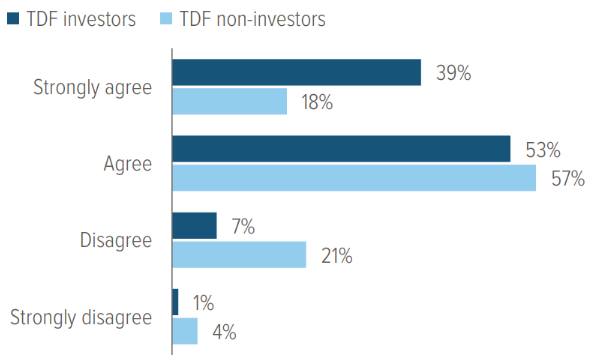

The same pattern appears when participants consider retirement more broadly. Ninety‑two percent of TDF investors agree that having a TDF increases their confidence in having a successful retirement, compared with 75% of non‑investors (Exhibit 3). Strong agreement is 39% versus 18%.

As of April 2025. Source: Voya IM.

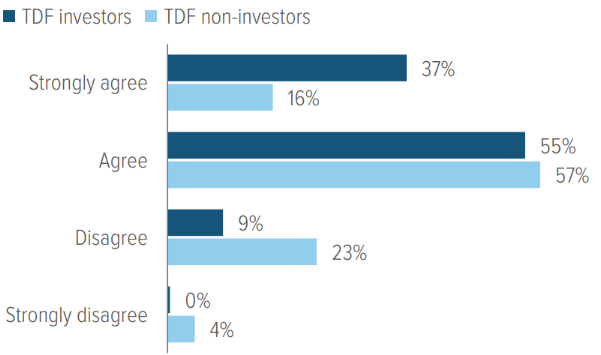

Stress tells a similar story. Ninety‑one percent of participants who invest in TDFs agree that doing so alleviated the stress of retirement planning, compared with 73% of those who don’t (Exhibit 4). Strong agreement: 37% versus 16%.

As of April 2025. Source: Voya IM.

These differences don’t mean that a single investment vehicle solves every retirement challenge. What they do suggest is that decision simplification and professional management are associated with higher confidence and lower stress.

Importantly, these outcomes don’t happen because participants become better investors, but because fewer high‑stakes choices are pushed back onto them. This is where Financial Literacy Month becomes genuinely useful—just not in the way it’s typically framed.

For DC specialists, April isn’t simply an education moment. It’s an opportunity to help sponsors ask a more revealing question: Does our DC plan build confidence by design, or does it require participants to figure too much out on their own?

That shift changes the conversation. Instead of debating how much information employees need, DC specialists can talk about plan architecture, such as defaults, framing, simplification, and professional oversight.

Most plans already offer education, but fewer offer coherence. DC specialists can stand out by using Financial Literacy Month to make that distinction clear. They help sponsors understand that accumulation metrics indicate whether a plan is functioning, but that confidence can underlie whether the plan feels manageable to participants—and whether they believe they’re making sound choices.

Participants don’t need to know everything, but they do need to trust the path their plan sets for them. DC specialists who help sponsors design for that trust aren’t dismissing financial literacy; they’re redefining it—around reassurance, clarity, and outcomes participants can reasonably expect to achieve.

A note about risk: There is no guarantee that any investment option will achieve its stated objective. Principal value fluctuates and there is no guarantee of value at any time, including the target date. The “target date” is the approximate date when an investor plans to start withdrawing their money. When their target date is reached, they may have more or less than the original amount invested. For each target date portfolio, until the day prior to its target date, the portfolio will seek to provide total returns consistent with an asset allocation targeted for an investor who is retiring in approximately each portfolio’s designated target year. On the target date, the portfolio will seek to provide a combination of total return and stability of principal. Stocks are more volatile than bonds, and portfolios with a higher concentration of stocks are more likely to experience greater fluctuations in value than portfolios with a higher concentration in bonds. Foreign stocks and small- and mid-cap stocks may be more volatile than large-cap stocks. Investing in bonds also entails credit risk and interest rate risk. Generally, investors with longer timeframes can consider assuming more risk in their investment portfolios.