Growth vs. Inflation

CIO, Multi-Asset Strategies and Solutions

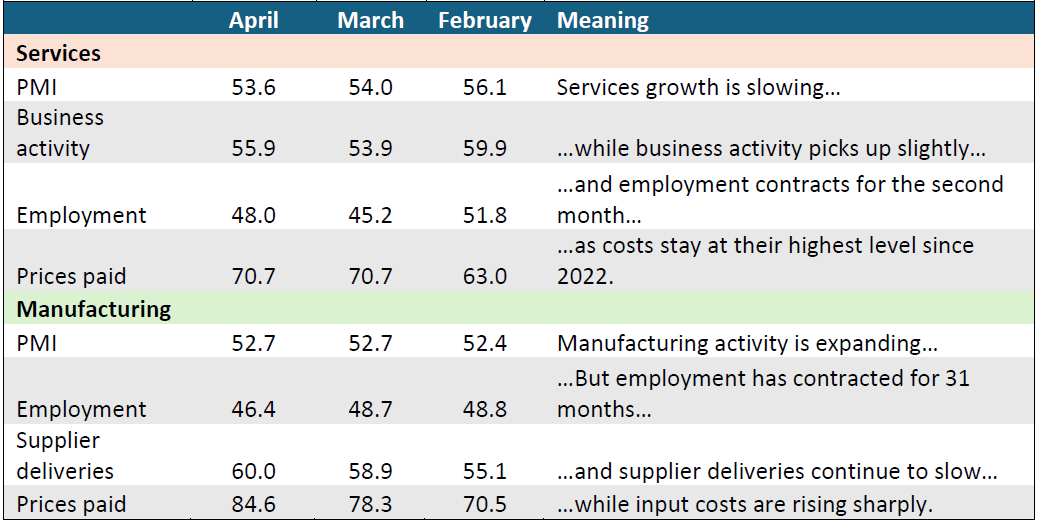

Recent economic releases point to slowing momentum in U.S. growth. This week’s ISM survey data shows that while activity remains in expansion territory, demand indicators have softened, reflecting more cautious business conditions. Ongoing uncertainty tied to geopolitical conflict and trade policy continues to weigh on confidence, while the lagged impact of earlier monetary tightening is still restraining investment and hiring. These headwinds point to softer growth dynamics, even if outright contraction is avoided. Here’s what’s in the numbers, and where they might hit your portfolio.

As at 05/06/26. Source: ISM. Note that "Supplier deliveries" is a category where higher numbers mean lower deliveries. For all other categories, higher numbers mean expansion or increase.

At the same time, inflation pressures remain evident. ISM PMIs continue to signal elevated pricing pressures, with the Prices component in both manufacturing and services remaining high.

This is reinforced by producer price data, which points to ongoing pressures tied to energy, transportation, and materials costs. Inflation dynamics are also being supported by periods of easing financial conditions, providing a modest tailwind to pricing pressures.

The resulting backdrop presents a difficult landscape for policymakers. Slowing growth could limit second round inflation effects, particularly if demand continues to cool. However, inflation remains above target and is supported by cost pressures and relatively accommodative financing conditions. As a result, policymakers face a trade-off between emerging growth headwinds and persistent inflation risks.

For investors, this potential slowdown amid higher input costs argues for a tilt towards higher quality exposures with pricing power, while maintaining diversification across assets that can navigate both slower growth and elevated inflation.

Julia Rozenfeld contributed to this article.