As the stock market rally faces fresh uncertainty, another trend is emerging: margin debt is on the rise.

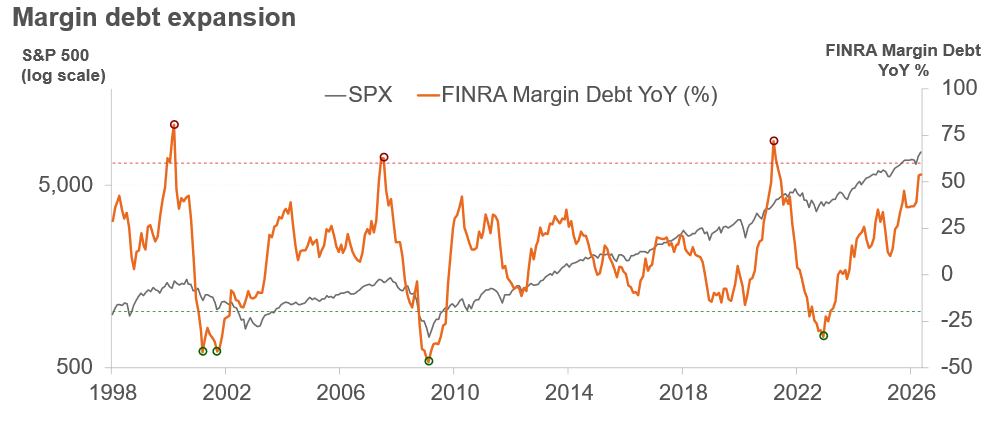

Data from FINRA show that investors are adding borrowed exposure at a faster pace, rapidly approaching levels last seen in 2021. That’s not territory you generally want to occupy.

Past extremes in 2000, 2007, and 2021 all appeared near speculative market peaks and were followed by large drawdowns.

Useful? Yes. Precise? No.

Margin debt isn’t a forecast. It doesn’t call the top, and it can appear quite early. In 2021, the margin debt signal appeared in March, but the S&P 500 continued to move higher before peaking in January 2022.

That timing gap matters because margin debt tends to rise with the market. Here’s how it (typically) works:

- Higher stock prices increase portfolio values.

- Larger portfolios create more borrowing capacity.

- More borrowing can add to buying pressure.

- Buying pressure pushes stocks higher.

That loop can keep working for a while, which is why rising margin debt often looks harmless—until it doesn’t.

The chart below shows how earlier problem periods occurred when margin debt started rising faster than the market itself, suggesting investors were adding exposure beyond what higher prices alone would explain. Today’s reading isn’t at those prior extremes, but it’s close.

As of 05/31/26. Source: Bloomberg, FINRA

What should you discuss with clients?

Start by framing rising margin debt as a risk indicator, not a market call. It doesn’t mean stocks are about to fall, but it does suggest that investor confidence, leverage, and exposure may be building at the same time.

For clients who have grown more comfortable with equity risk during the rally, this is a timely prompt to revisit portfolio assumptions: How much downside they can tolerate? Have recent gains increased concentration? Does the current allocation still reflect their time horizon and liquidity needs?

The practical takeaway is not to de-risk reflexively, but to avoid letting momentum do the portfolio construction. Diversification won’t prevent losses, but it can help reduce the risk that too much of a portfolio is exposed to the same market driver at the same time.